Retirement Income FAQs

Your retirement income questions, answered

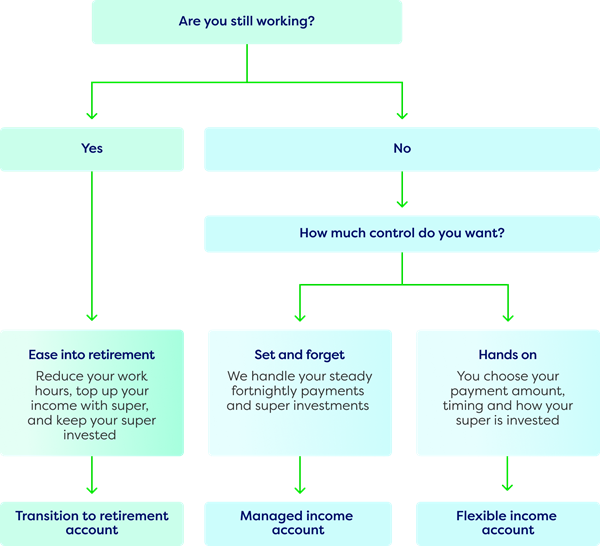

Start with our quick decision guide to see which option may suit you. Then explore our FAQs to understand how each account works and how to make confident choices for a happy and confident retirement.

Not sure where to start?

Use this quick guide to find the right retirement income account for you. Still working? This assumes you’re under 65.

Now, meet your account

You’ve discovered which option may work best for you. Here’s where you can learn more.

Support to help you decide

If you’d like to talk through whether a retirement income account is right for you, our super experts can walk you through what to expect and how it works.

Retirement Income FAQs

A retirement income account lets you turn your super into a regular income during retirement while your money stays invested. It gives you the confidence to plan your lifestyle and still access your super when you need it.

Managed Income account: Provides predictable, regular payments and while your super remains invested, so you can enjoy a steady income with peace of mind.

Flexible Income Account: Gives you more control over how much and when you withdraw, as well as choice over investments while your super remains invested.

Anyone who's:

- Between 60-65 who has retired or stopped working for an employer, or

- 65 or over (even if working).

Then, transfers at least $20,000 from your super account into your Managed Income account.

If you’re between 60 and 65 but haven’t met the criteria, you might be able to start accessing some of your super with a Transition to retirement strategy.

Yes. You can transfer super from other funds into your CareSuper account before opening your retirement income Account. This simplifies managing your money and helps you keep track of your investments and insurance.

Before combining your super into CareSuper you should consider whether this is right for you and check for fees, costs and performance. You should also check the impact on any insurance arrangements (such as loss of insurance) or other benefits.

Managed Income account: Payments land in your bank account fortnightly, so amounts remain stable for peace of mind.

Flexible Income account: You can choose to receive payments weekly, fortnightly, monthly, quarterly, or annually.

Managed Income account: Payments are set to fortnightly, so amounts remain stable for peace of mind.

Flexible Income account: You can increase, reduce, or pause payments to suit your circumstances.

Any remaining balance in your account will be paid to your nominated beneficiaries, or your estate or others who may be entitled depending on your circumstances. This ensures your super continues to support your loved ones.

Yes. Our fees cover everything needed to manage your income account; from administration to investment and transaction costs, so your retirement savings are looked after efficiently and transparently.

Yes, you can withdraw extra money whenever you need to cover bills, holidays or big purchases. Although it may reduce future payments and how long your income will last.

It’s easy, read the Retirement Income PDS, complete the application form at the end, and return it to us. If you’re combining super from other funds, make sure it’s all in your CareSuper account first. Call one of our super experts on 1800 005 166 or book a call-back if you need help.

Are you retirement ready?